Refinancing a mortgage in Ohio especially in Ross County can feel confusing when rates change daily and lenders give mixed advice. Many homeowners want lower payments or a shorter loan but don’t know whether refinancing is financially worth it.

This guide explains everything specifically for Ross County homeowners, including break-even calculations, local refinance factors, costs, timelines and common mistakes so you can make a confident, numbers-based decision.

Is Refinancing Even Worth It for Me Right Now?

The first step is determining your break-even point the time it takes for monthly savings to cover refinancing costs. For example, a Ross County homeowner with a $250,000 mortgage at 6.5% considers refinancing to a 5% rate. With $3,600 in closing costs and $150 monthly savings, the break-even point is 24 months. Refinancing makes sense if you plan to stay in your home longer than that. Refinancing is generally not recommended if you plan to move soon, your closing costs are disproportionately high, or you cannot secure a lower interest rate. Calculating your break-even point ensures your decision is grounded in numbers rather than vague advice.

How the Ross County Housing Market Affects Refinance Decisions

Home values in Ross County have shown steady growth over recent years, which makes refinancing more attractive for many homeowners. When home values rise, equity increases, making it easier to qualify for lower rates or cash-out options.

However, neighborhoods with slower value growth may see different appraisal outcomes, so Ross County homeowners should always compare their home’s estimated value before applying. A strong appraisal leads to better rates, lower fees, and more refinance options.

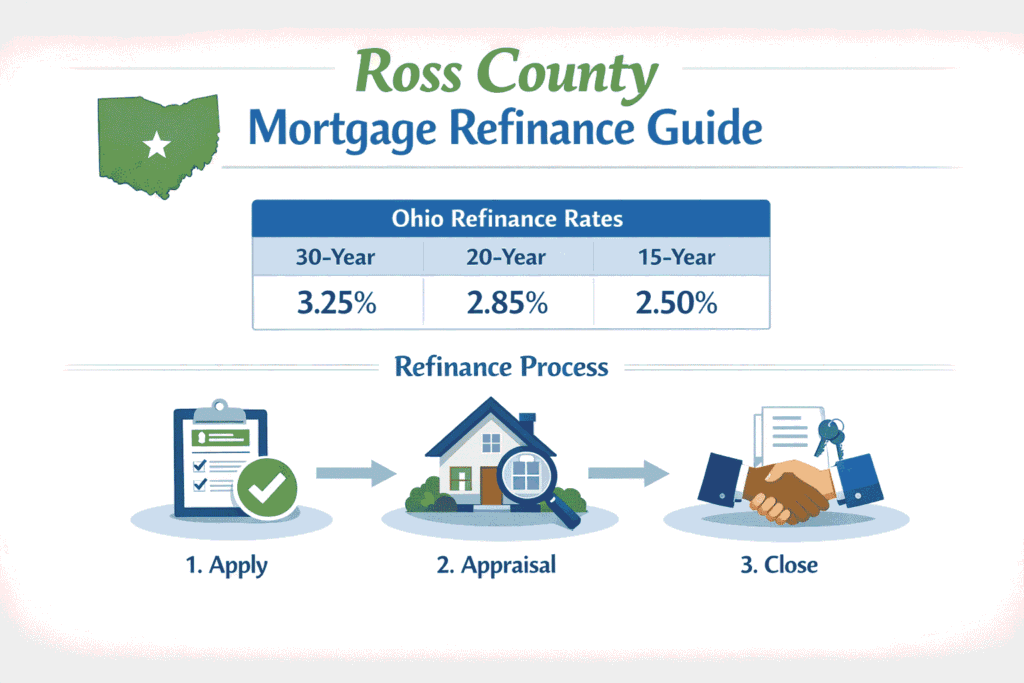

What Are the Current Mortgage Refinance Rates in Ohio?

Mortgage rates vary by county and lender. Ross County homeowners cannot rely on national averages because local housing trends, property taxes and lender risk assessments affect rates. As of early 2026, average Ohio refinance rates are:

| Loan Type | Average Rate | Typical Term |

|---|---|---|

| 30-Year Fixed | 5.0% | 30 years |

| 20-Year Fixed | 4.75% | 20 years |

| 15-Year Fixed | 4.25% | 15 years |

Rates differ even within Ohio due to factors like local property values, insurance requirements, and lender volume. They can also change daily. Monitoring rates regularly helps you choose the optimal time to refinance without overpaying.

How Much Will Refinancing Actually Cost Me?

Refinancing includes several costs that homeowners often overlook. Typical Ross County fees include:

- Closing costs: 2–5% of loan balance

- Appraisal fees: $300–$500

- Lender fees: $500–$1,000

- Title and recording fees: $200–$600

For a $250,000 mortgage, total costs usually range from $5,000 to $10,000. Understanding these fees is crucial because they directly affect your break-even point and overall savings. Being transparent about costs prevents unpleasant surprises during the refinancing process.

| Cost Type | Typical Amount | Notes |

|---|---|---|

| Closing Costs | 2–5% of loan amount | Higher for cash-out refinances |

| Appraisal Fee | $300–$500 | Based on property size & area |

| Lender Fees | $500–$1,000 | Varies by lender |

| Title & Recording Fees | $200–$600 | Paid to Ross County Recorder |

| Credit Report Fee | $30–$60 | Required for all lenders |

Will Refinancing Lower My Monthly Payment or Just Reset My Loan?

Refinancing can reduce monthly payments, shorten the loan term, or provide both benefits. Choosing the right option requires understanding the trade-offs between immediate savings and long-term interest costs. Shorter terms save interest but increase monthly payments; longer terms reduce monthly payments but extend interest accumulation. It’s important to evaluate the financial impact carefully and align it with your long-term goals.

Can I Refinance with Bad or Average Credit in Ohio?

Homeowners with average or low credit scores still have refinancing options. Conventional loans typically require a minimum score of 620, FHA refinances accept scores as low as 580, and VA or USDA programs may offer flexibility for eligible homeowners. Preparing all financial documents, paying down debt, and avoiding new credit lines prior to refinancing increases your chances of approval.

How Much Home Equity Do I Need?

Home equity is the portion of your home that you actually own, and it affects what type of refinance you can do. Most rate-and-term refinances work best if you have at least 20% equity in your home, while cash-out refinances usually require a bit more. In simple terms, the more equity you have, the better your chances of getting a good interest rate and loan terms. If you’re planning a cash-out refinance for renovations or debt consolidation, make sure you have enough equity to qualify and avoid higher costs.

How Long Does the Refinance Process Take in Ohio?

The average Ohio refinance timeline is 30–45 days, depending on document completeness and appraisal scheduling. The process involves submitting an application, lender review, appraisal, underwriting, and final closing. Delays often occur if documents are incomplete or appraisal scheduling is slow. Preparing early and providing all documentation upfront helps avoid unnecessary delays.

Should I Choose a Local Ohio Lender or an Online Lender?

Local lenders offer familiarity with Ross County property values and personalized service, while online lenders may provide slightly better rates and faster approvals. Homeowners who value guidance and local insight often prefer a local lender, while those focused solely on rates may opt for online lenders. Evaluating the balance between rate, service, and expertise is crucial for a smooth refinance experience.

How Refinancing Affects Property Taxes in Ross County

Refinancing does not change your property tax rate, because taxes are based on county-assessed value, not your mortgage.

However, your escrow payment may change if your lender recalculates taxes and insurance after refinancing. Ross County property taxes are billed semi-annually, so lenders adjust escrow to match the county’s billing schedule.

Cash-out refinances may increase escrow slightly because lenders want enough cushion to cover upcoming tax cycles

Choosing the Right Refinance Program in Ross County

Not all refinance programs are the same, and selecting the right one depends on your goals. Homeowners looking for lower monthly payments may prioritize a 30-year fixed refinance, while those aiming to save interest prefer a 15- or 20-year loan. Veterans can explore VA streamline options and rural homeowners may consider USDA refinance programs. Local Ross County lenders often provide guidance tailored to the county’s housing market, property taxes and appraisal trends, helping you select a program that balances affordability, risk, and long-term savings.

Who Should NOT Refinance in Ross County

Refinancing may not be a good idea if:

- You plan to sell your Ross County home within 1–2 years

- Your closing costs are too high compared to expected savings

- You cannot secure a lower rate or shorter term

- Your home’s value may not appraise high enough

- You recently refinanced and would reset the loan term again

Avoiding these situations protects homeowners from unnecessary costs.

Common Refinance Mistakes to Avoid

Ross County homeowners often make mistakes that reduce refinancing benefits: ignoring closing costs, accepting the first rate offered, refinancing too soon, or skipping a full appraisal or title review. Red flags include lenders pressuring you to sign, unclear fee disclosures or promises of unrealistically low rates. Following a checklist ensures a safe refinance:

Checklist – Key Steps:

- Compare at least three lenders for rates and fees

- Calculate your break-even point including all costs

- Verify fees in writing

- Ensure eligibility based on credit score and equity

- Review local property taxes and insurance

Conclusion

Refinancing in Ross County, Ohio can lower payments, shorten loan terms, or provide cash for home improvements or debt consolidation. Calculating the break-even point, comparing local and online lenders, and understanding fees and eligibility ensures homeowners make informed decisions. With careful planning, refinancing can turn uncertainty into financial advantage.

FAQs

1. How often do Ohio refinance rates change?

Rates can change daily and sometimes multiple times per day, depending on lender adjustments and market conditions.

2. Do I need an appraisal for every refinance?

Most refinances require an appraisal, although some streamline or VA loans may waive it.

3. Can I refinance multiple times?

Yes, but frequent refinancing can reset your loan term and may increase total interest if not planned carefully.

4. Can refinancing help me consolidate debt?

Yes, a cash-out refinance can pay off high-interest debts, but it increases your mortgage balance and should be done cautiously.

5. How long does it take to close a refinance in Ross County?

Typically 30–45 days, depending on the completeness of documents, appraisal scheduling, and lender workflow.

Does refinancing increase property taxes in Ross County?

No. Refinancing does not increase or decrease property taxes. Taxes are based on your property’s assessed value set by the Ross County Auditor, not your mortgage. Only your escrow payment may change.